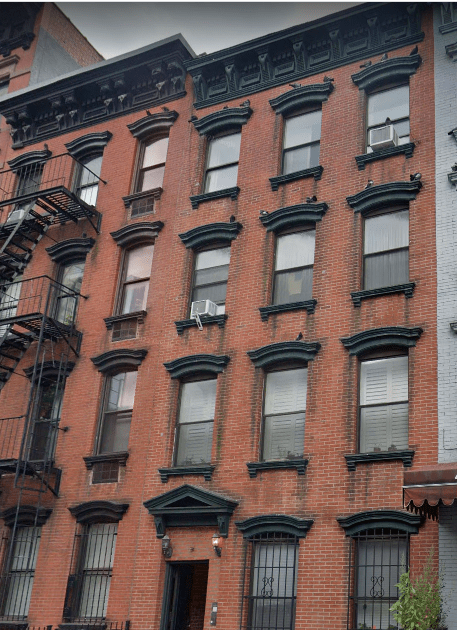

THE HISTORY

Beginning in the 1970s- when New York City was in financial turmoil- many building owners stopped paying property taxes and allowed their buildings to fall into disrepair as the costs to renovate and maintain outweighed the rental income forcing countless owners into bankruptcy.

As the buildings sat in a state of abandonment the city chose to offload the burden of managing so many properties and began offering the sale of individual units- restructured as HDFC cooperative apartments- to tenants (renters) living in the buildings. These units were initially sold for $250 and included a property tax incentive, but came with the responsibility of renovating, managing, and maintaining a property that would often end up taking years to turn around.